![]()

- Introduction

- A bit of History

- Company financials

- Business segments, competitive advantage and competition

- Risks

- Valuation

- Summary

Introduction

Kri-Kri Milk Industry is engaged in the production, distribution and sale of ice cream and yogurt. This Greek company was founded in 1954 by the Tsinavos family, which still manages the company and owns 73% of the business. The headquarters and main production facilities and distribution centre are located in Serres, in the north of Greece. A secondary distribution centre is located in Attica, in the south of Greece.

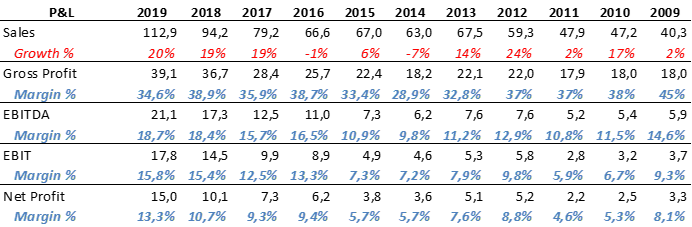

In 2019, the company achieved 113M€ in sales and exports were 41% of that figure. The company exports its products (mainly yogurt) to more than 25 countries, with UK and Italy being the biggest export markets. EBIT margin is around 15%.

The company was listed on the Athens Stock Exchange in 2003. Since then, sales have grown at a compounded annual growth rate (CAGR) of 13,4%. From 19,5M€ in 2003 to 113M€ in 2019.

At 6,30€ per share, the current market capitalization is 209M€. I have been invested in Kri Kri for some years now and, although the stock has become better known since they started publishing the reports in English, I still consider it has a nice upside potential. Perhaps because investors are still afraid of investing in Greece, who knows.

A bit of history

In 1954 George Tsinavos founded the company establishing a small pastry shop in Serres (Greece) with a variety of ice-creams. During the early years the company focused on ice cream production and delivery in the local market. In 1995 starts distribution in Athens and by the end of the 90’s they start the Greek yogurt production and expansion to international markets.

In December 2013, a fire broke out on the yogurt production plant in Serres, causing considerable damage. In less than 8 months, they buit a new yogurt plant which was more efficient and had twice the capacity of previous plant. During this period were they couldn’t produce yogurt by themselves they outsourced all the production. They had some supply chain problems and temporary lack of stock, however, yogurt sales only decreased an 11% that year.

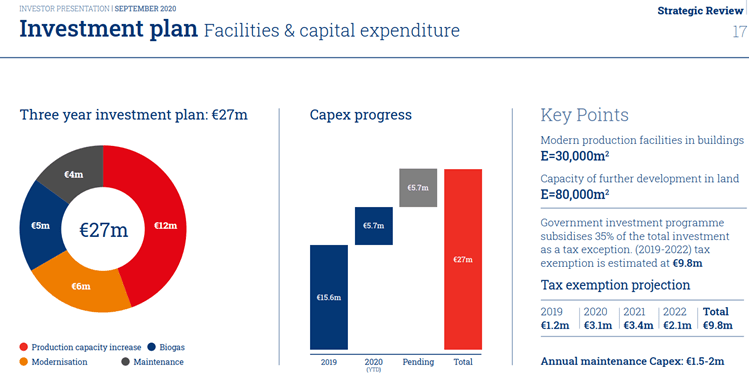

In 2019, the company presents a new three-year investment plan of 27M€ in order to expand the production capacity in yogurt and ice cream.

Company financials

Income statement

Debt

Investments

For the last several years, the company has developed investment projects to increase production capacity as well as technological upgrading of both yoghurt and ice cream factories.

In the following table we can see that, for the last 7 years, investments have significantly outpaced depreciation & amortization.

In the 2014 investment figure, there is the 20M€ investment in the new yogurt plant that they had to build because the fire that I mentioned previously.

In 2019, they started a new investment plan of 26,6M€.

Suppliers

The company has no significant dependence on any supplier. Any supplier represents more than 10% of total purchases.

Proximity to farms allows them to deliver products with daily fresh milk.

Credit risk

Receivables of specific supermarket chains are credit insured with a contract covering credit losses, occurring from insolvency, up to 90%.

Receivables from foreign customers, are credit insured with a contract covering credit losses, occurring from insolvency, up to 95%.

Business segments, competitive advantage and competition

The company has 4 business lines:

- Yogurt Greece

- Yogurt Export

- Ice cream Greece

- Ice cream Export

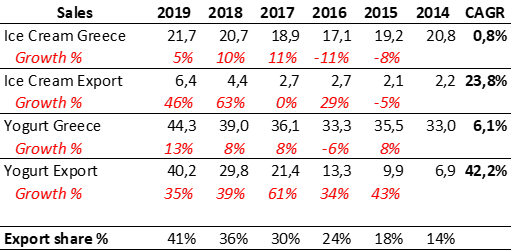

The following two tables show where the growth is coming from:

As you can see, in 2019 exports were already 41% of revenue. Yogurt exports, the growth driver, is already 36% of total revenue. The yogurt division (Greece + Export) is 75% of sales.

Now we will have a look at each division, which I think is important to understand the business, including possible competitive advantages and competition landscape.

Yogurt Greece

This division represents 39% of total sales. Approximately, 70% of sales are branded products and 30% is private label. The company claims that one in four Greeks consume yogurt produced by Kri-Kri (between branded + private label).

To keep the division growing, the company is additionally focusing on profitable niches:

- Healthy product line – high protein and super foods

- Special formula for silver age

- Lactose free products

- Kids and infant product category

In branded yogurt they are the second largest producer in Greece. They have 96% brand awareness and are sold in 100% of Greek supermarkets.

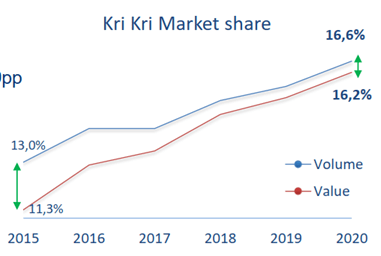

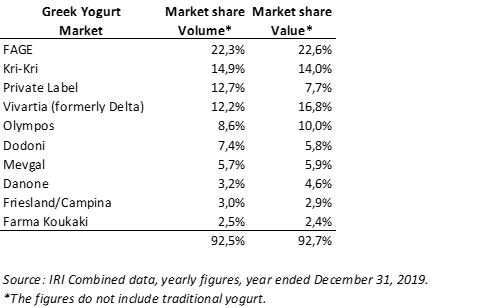

Market share in branded yogurt:

Looking through the company presentations we can see that in terms of volume, they have gone from 4% market share in 2008 to 16,6% market share in 2020. I think this is very remarkable taking into account that Kri Kri started its yogurt production in the 90’s. I looked into the competitors websites and found that Fage, Vivartia (Delta) and Mevgal started their yogurt operations in 1964, 1994 and 1974, respectively.

At the end of 2019, this was the split of market share by player:

In terms of private label yogurt, Kri Kri has a 70% – 80% market shre.

Insights and competition (Yogurt Greece division)

Before the insights, I would like to make the differentiation between authentic Greek yogurt and Greek style yogurt. You can only say Greek yogurt of its made in Greece, with Greek milk. Greek style yogurt is not made in Greece. This is important for later when we have a look at the yogurt export division.

Going back to the Yogurt Greece division, I believe that Kri Kri is the lowest cost producer of Greek yogurt. You can see this by their market share in private label in Greece, which is 70-80%. Actually, they started the private label greek yogurt concept in Greece. Perhaps we could think that Greek supermarkets choose Kri Kri because they make the best quality yogurt. Well, with so many old and family owned Greek yogurt manufacturers I don’t think so. Obviously Kri Kri product is good, otherwise wouldn’t have this branded yogurt market share, but I definitely think supermarkets choose Kri Kri for private label because they are the cheapest. This is where the yogurt export success comes from (more on this later in Yogurt Export).

In relation to branded yogurt, could Kri Kri continue to increase its market share? I don’t know, but from my research and from what the Company told me a year ago, it results that the Greek competitors I put on the table before are very leveraged or have much lower margins, or both. I think this has been already an advantage for Kri Kri and probably will continue to be going forward. According to Fage and other sources, competition in the Greek yogurt market in Greece (and abroad too) is ferocious. This will be very tough for leveraged and/or lower margin competitors. Additionally, the leveraged and low margin competitors invest less money in new equipment or R&D, which makes them more vulnerable and Kri Kri already takes advantage of it and I believe will continue to do so.

Let’s have a look:

Fage: Is not a public company, but since they are financed in the capital markets they have to publish almost the same information as if they were listed, so you have annual and interim results in their website. What do we see? Sales in 2019 and 2018, went down 10% from previous year, which might indicate a serious sales problem, since Greek yogurt market overall is growing nicely. In 2017 (I haven’t gone further), they had 18,7% EBIT margin, but last two years has gone down to 10%. Current Net Debt / EBITDA ratio is 3x. Kri Kri has no debt.

Vivartia: This company was owned by listed Greek investment holding company Marfin Investment Group and has just been sold to the well known private equity firm CVC. Net Debt / EBITDA is 6x, which I think is too much even for a food company.

Mevgal: Kri Kri told me that they have 2 – 3% net profit margins. Kri Kri has more than 10% net profit margin.

I would also like to mention that in relation to branded yogurt, if they have been gaining so much market share is because of the quality of the products and continuous innovation, not price, which is the success factor in private label.

Yogurt Export

Approximately, 82% of sales is private label and 18% is branded products.

Around 60% of total sales is UK and 25% – 30% Italy. Then comes Germany and Sweden.

All their clients are supermarkets.

Private label offers a strategic way to enter markets of interest with lower entry cost and build relationships. The strategy going forward is to expand the private label products portfolio and place branded products to existing customers.

Authentic Greek & Greek style yogurt market in its main export markets:

Italy: 148M€

UK: 305M GBP

Germany: 162M€

Other markets the company considers for geographical expansion: France, Spain and Russia.

Insights and competition (Yogurt Export division)

This division has been the growth driver of the company for the last 6 years and is expected to continue to be for the following years. The success of this division has come from the increased demand of Greek yogurt in developed countries for the last several years.

According to the IMAC Group, a market research company:

One of the key factors driving the global Greek yogurt market is the increase in health consciousness among consumers and change in dietary preference towards healthy and nutrient-rich food products. Owing to the increasing consumption of fat-free and weight management products, Greek yogurt has gained immense popularity among consumers.

So, how has the company gone from 2,4M€ in export yogurt sales in 2008 to 40,2M€ in 2019?

Kri Kri success in yogurt exports comes from the willingness of European supermarkets to have a private label authentic Greek yogurt product. Being (I believe) the lowest cost producer, as I mentioned before, is what has made Kri Kri so successful selling yogurt abroad.

But why are they the lowest cost producer? According to the company the main reason behind this is (1) the state of the art facility for yogurt production facility they built from scratch in 2014, after the fire that took place in 2013, and (2) easy access to considerable supplies of milk. Apparently, Greek competitors production plants are very old an much less efficient and automated than the production plant of Kri Kri. The good news going forward is that this advantage versus competitors might continue, because low margin and very leveraged competitors might not be able to afford a new plant, at least not all of them for sure. Fage, with 3 times Net Debt / EBITDA will build a new plant in Luxembourg, but the good news is that Fage is not into private label.

Another think that reassures me that they are the lowest cost producer is that from one of the conversations I had with the company they said that Vivartia and Mevgal, which are the ones competing in Europe with private label, are having a hard time to compete in price. The company also mentioned that when they lose a private label contract is not normally because they lose to a Greek competitor, but because they lose to a Greek style yogurt manufacturer. This is the case in Germany so far, according to them. Apparently, in UK and Italy they have been so successful because supermarkets there prefer to offer authentic Greek yogurt. The good news is that there are other markets were consumers prefer authentic Greek yogurt too.

Perhaps a company that is growing selling private label yogurt might not appeal to some investors, but keep in mind that they have 15% – 19% EBIT margins in the Yogurt Export division.

One more thing. Having this new yogurt production facility is also very important for exports for other reasons. Companies like Aldi and Lidl do a very thorough work before they start to work with a supplier. One of the things they do before starting a collaboration with a new supplier is to visit the manufacturing plant, warehouse, etc. I am sure they will not find the same quality of facilities if they go to visit the other Greek yogurt producers. European supermarkets know that if a supplier works with Aldi and Lidl is because it has ticked all the boxes. Kri Kri acknowledges that this has been a plus when starting conversations with a new supermarket.

Ice cream Greece

In 2019, this division represented 19% of total sales. They are the only Greek ice cream company with nationwide sales network. Points of sale: 16.000 in 2019, 15.000 in 2018, 14.000 in 2017.

They do branded and private label as well. Branded products are sold to Horeca channel and supermarkets through local distributors. Private label products are sold directly to supermarkets.

The market size is 223M€. The ice cream market in Greece, like in all developed countries, is already consolidated. They have 96% brand awareness and are the third largest player in terms of volume. The first competitor is Unilever, with a 24,4% market share. The second player is Froneri (former Nestle), which has 21,4%. Kri kri has 14,9% market share.

The strategy is to continue to increase points of sale, maintain high profit margins level and to capture any Private Label opportunity. Currently, 70% of sales is branded products and 30% is private label.

Insights and competition (Ice cream Greece division)

What I will say here is not an insight because I think is broadly known. Ice cream markets in developed countries are very consolidated. In Europe, for example, there are usually three brand names, Nestle and Unilever and a local brand. In Greece is the same. Between these three companies they have 61% market share (by volume).

Therefore, is like a natural oligopoly with stable market shares where the players, in general, do not get involved in cutting prices to win market share. In the Ice cream division, Kri Kri has 50% gross profit margin and 18% – 19% EBIT margin.

Here the competitive advantage is the brand and the nationwide distribution network, which makes it very difficult for new entrants.

Ice cream Export

In 2019, this division represented 6% of total sales. Ice cream exports are booming too, although from a very low base.

The company believes they have an opportunity to continue to increase ice-cream exports, within the private label segment, very rapidly (I asked also to the company what happened this year, because they are down big). The European ice cream private label market is 10b USD. Their clients in private label are ice cream companies and supermarkets.

I believe they have an opportunity to grow strongly at the beginning just by offering private label ice-cream to the same supermarkets that buy their yogurt. I believe some of them will go with Kri Kri. Moreover, Unilever and Nestle are not interested in making private label ice cream. A part from that, I need to dig deeper in this business segment. I don’t know who the players are in this space.

The branded product strategy is to continue to build the distribution network (like in Greece) in countries with proximity: Cyprus, Albania, North Macedonia, Iraq. They already have 5.000 points of sale. My guess is that in these markets, the ice-cream sector is not yet consolidated.

Risks

I just will copy a slide from one of the company’s presentations. I also consider these to be the main risks.

Valuation

Number of shares (in millions): 33,1

Stock price 03/12/2020: 6,28 €

Market Cap: 208M€

Valuation assumptions:

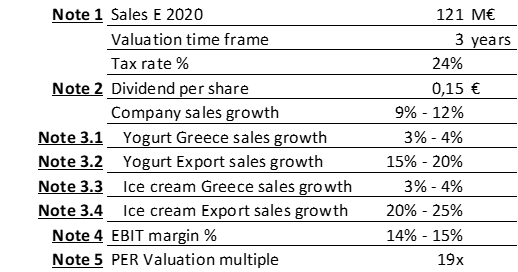

Note 1: Considering the interim results, I consider that 121M€ for 2020 is reasonable. It implies a 7,5% increase vs 2019.

Note 2: I picked up the 2018 dividend per share. In 2019, actually, it was already 0,18€ per share.

Note 3.1: Since they have achieved a 6% CAGR for the last 6 years, I consider a 3-4% to be reasonable. We can see the growth they have had for the last 6 years in a table at the beginning of the Business segments section.

Note 3.2: CAGR for the last 6 years has been 42%. The last 2 years has been growing 35%. The company thinks the rate growth will slow down going forward but still above 20%. I consider a 15% – 20% growth to be reasonable for the next 3 years.

Note 3.3: CAGR for the last 6 years has been +0,8%. We can see the growth they have had for the last 6 years in a table at the beginning of the Business segments section. We see that for the last 3 years the division has grown nicely.

Note 3.4: We can see the growth they have had for the last 6 years in a table at the beginning of the Business segments section. I consider a 20% – 25% growth to be reasonable, although I would like to comment with the company, as I said before, about the decrease they are having this year. I believe it’s a temporary think. Actually, in the yogurt export division they also had a decrease in sales in 2014. Even a company that is growing sales strongly for a long period of time, the sales graph is not always is a straight line.

Note 4: The company is already making 15%+ EBIT margins. I believe that a range of 14% – 15% is reasonable.

Note 5: As we see in the table below, the peer group trades at 21x. For this reason I consider that choosing 19x valuation multiple for Kri Kri is reasonable. Perhaps, one could consider that since is a tiny company compared to these mega giants, it deserves an even lower multiple. Well, I already put a lower multiple for this reason, but we have to consider that these big companies are essentially not growing and, with the exception of Emmi, all have much higher levels of debt than Kri Kri. Actually Kri Kri, has no debt.

Therefore, I estimate that Kri Kri Milk upside potential is 59% – 83%, which implies an IRR of 16% – 22% (including dividends).

Summary

- No debt.

- Strong balance sheet (equity = 62% of total assets)

- Family owned company.

- Defensive business with good growth.

- High EBIT margins, in spite of doing a lot of private label yogurt and ice cream.

- Increasing capacity for yogurt and ice cream production.

- Lowest cost producer of (authentic) Greek yogurt. This has made the Yogurt export division to be the growth engine of the company, selling private label authentic Greek yogurt for European supermarkets. Strong growth will very probably continue for some years.

- Largest producer of yogurt in Greece: 25% market share by volume (branded + private label). They have 70 – 80% market share in private label. Market share in branded yogurt (volume) has gone from 4% in 2008 to 16,6% in 2020.

- Second player in Greece after Nestle in ice cream. Consolidated and stable market. Kri Kri has 50%+ gross margins in this segment.

- Opportunity to have a piece of the 10B USD ice cream private label market in Europe.

Links of interest:

Disclaimer: The purpose of this blog is not to provide financial advice or recommendations to buy or sell specific investments. Please, do your own research before making any investment decision. If you are unsure of any investment decision, you should seek a professional financial advisor.

19 thoughts on “Analysis of kri kri milk industry”